Withdrawing From RRSP and TFSA For Retired Canadians in 2026

My article on Withdrawing from your RRSP and TFSA as a retired Canadian has grown as I’ve updated it over the years. The most detailed version of it can be found here in my DIY Canadian retirement planning course. I’ve used 2026-updated limits and details for your RRSP and TFSA in this most recent update.

After writing a deep dive article on whether the 4% safe withdrawal rate still works for retirement at various ages, I received a lot of questions basically asking:

“Ok, so 4% is a good rule of thumb, but when I actually go to withdraw money from my various investment accounts, to put into my chequing account & high interest savings account in order to pay for day-to-day expenses, what is the best way to avoid taxes?”

Upon reading many of these types of questions, I realized that I wasn’t actually 100% sure how to optimize withdrawing from my RRSP and TFSA in order to keep the most money in my hands as I nibbled down my nest egg over the years.

I had some notion of things to stay away from when withdrawing money in retirement, but while there is a ton of information out there on how to build assets using one of Canada’s online brokerages or robo advisors, there wasn’t a lot out there for folks looking to drawdown their assets in an efficient manner.

The dirty secret for this imbalance?

There is no money in telling people how to cash out of their investments!

Upon making this realization, there was only one thing left to do – create the ultimate resource for Canadians looking to withdraw from their TFSA and RRSP in retirement (aka: Draw down their nest egg) in as efficient a way as possible after they had built it up, and hit their “magic 4% rule” number.

In order to be as thorough as possible, I recruited my friend Kornel Szrejber – who is actually living the Early Retirement + Withdrawal Life, to help me out in regards to optimizing Canadian tax efficient withdrawal strategies.

Best 2026 Broker Promo

Up To $2,000 Cash Back + Unlimited Free Trades

Open an account with Qtrade and get the best broker promo in Canada: $100 when you invest $1,000!

The offer is time limited - get it by clicking below.

Must deposit/transfer at least $1,000 in assets within 60 days. Applies to new clients who open a new Qtrade account by July 31, 2026. Qtrade promo 2026: CLICK FOR MORE DETAILS.

Introduction to Retirement Withdrawals for Canadians 2026

The goal with this resource is to explain to Canadians how to go about structuring their RRSP, TFSA, and Non-Registered accounts as they head into retirement, and how to weigh the tradeoffs involved for their specific situation.

This RRSP and TFSA withdrawal guide will NOT cover the “wealth building phase” of planning in-depth – although it’s definitely possible to keep growing your wealth as you enter retirement. In order to understand what we mean by “The 4% Rule” or “Save 25x Your Annual Budget Rule”, please download our free eBook: Can I Retire Yet?

If you want to rely on dividends to fund your retirement, we recommend checking out our Best Canadian Dividend Stocks or Best Canadian Dividend ETFs articles.

When we started to look at all of the different considerations for folks looking to take money out of investment accounts to fund retirement, we realized that there were many more variables than the average person might think.

It can be a little bit overwhelming!

So here’s what we decided to do: Start with the easiest wins, and then gradually work our way down to the “cherry on top” stuff – which would be nice to do, but which should be a lower priority. Then we’ll get to Kornel’s real-life example of how he has structured his TFSA and RRSP withdrawals to fund his day-to-day life.

Withdrawing from Your RRSP and TFSA: Taxable Income vs Non-Taxable Income

Most retirees have three main goals when it comes to drawing down their nest egg in retirement.

These goals differ slightly if we’re looking at a pre-55 retirement (what I would call “early retirement”) or a 55+ retirement – but they’re very similar in almost any situation.

- Pay as little tax as possible!

- Get as much money given to you by the government as possible! (Aka: reduce clawbacks on government benefits.)

- Leave my investments where they will grow the most – and be sheltered from the tax man – for the longest period of time.

In order to dig into those three goals, the first step is to understand what taxable income vs non-taxable income is.

Taxable Income = Any money coming to you that the government will say that you owe taxes on.

Earning money through wages, salaries, piecework or “gig work”, commissions, or rental income, are probably the most common forms of taxable income.

For the purposes of selling investments and withdrawing money from your investment portfolio however, it’s important to know that dividends and capital gains are also considered taxable income – although they have special rules.

Personal pension income is also considered taxable income. OAS and CPP are considered taxable pension income.

Non-Taxable Income = Any money coming to you that you have already paid taxes on, or which the government says that you don’t need to pay taxes on.

TFSA withdrawals, and certain government benefits are generally considered the main sources of non-taxable income. Now, it’s important to understand that not only is calculating your taxable income important to legally avoid paying unnecessary tax – but also to make sure that you understand what numbers the government will look at when they figure out how much Old Age Security (OAS), Guaranteed Income Supplement (GIS), and Canada Child Benefit (CCB) to send your way.

Understanding How Taxes Will Be Applied To Your Retirement Withdrawals

Every province is going to charge you a different tax rate on your taxable income, as they have their own unique tax brackets. As a rule of thumb though, most Canadian couples will aim to retire and have each partner stay under the $58,523 level of taxable income because income over that amount gets hit with a 20.5% federal tax rate instead of a 14% tax rate.

Note that the 14% tax rate is new for 2026, as it was 15% in that tax bracket before the Carney government’s changes.

Now some frugal retirees will say: “Forget that $117,000 in combined income mark – you don’t need it and can make due with significantly less! Why not retire earlier with a combined taxable income closer to the $50,000 mark?”

Now living on less than $50,000 per year isn’t every couple’s dream, but it CAN stretch surprisingly far if you focus on minimizing expenses, own your home, and/or using creative strategies like living somewhere really warm and cheap for part of the year (often called “geo-hacking” by the cool kids).

Here’s what Canadians need to understand about taxable income and withdrawals from their RRSP, TFSA, and non-registered accounts.

Taking money out of your RRSP = Taxable Income (Just as if you had earned it at a job).

Taking money out of your TFSA = Non-taxable Income = It’s all yours, taxes have been paid, not only is the cash you put in there tax-free when you take it out, but all the money it made while it was compounding is tax-free as well!

Taking money out of your Non-Registered Account – Some taxable income and some non-taxable income… it’s a bit more complicated. Non-tax-sheltered accounts owe taxes on the money they make each year.

The initial money that you used to purchase investments has already had tax paid on it. When you sell the investment to spend the money, the only amount of money that gets taxed is the capital gains that have accrued along the way.

Most Canadians will have all of their investments inside of their RRSP and TFSA, but if you have maxed those out and use a non-registered account instead, then you’ll need to really pay attention to taxation details.

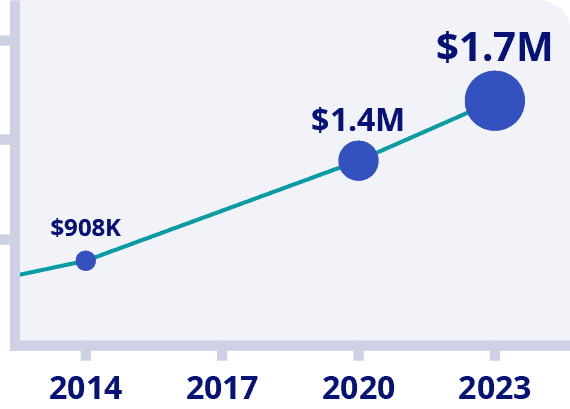

Are You Saving Enough for Retirement?

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Try Now With 100% Money Back Guarantee*Data Source: BMO Retirement Survey

How Are Dividends and Capital Gains Taxed Outside of RRSPs and TFSAs?

Ok, so when investments are placed inside of a tax-protecting RRSP or TFSA, they get to make money without the tax man reaching in to take any of it.

You can collect dividends, and buy/sell stocks/ETFs until your heart’s content, and you do not pay any taxes.

It’s a fantastic deal.

Outside of an RRSP or TFSA is a different story however – and in the interests of keeping this article below 67,000 words, we’re going to ignore RESPs, and RDSPs for now.

If you want to retire early, maxing out your RRSP or TFSA isn’t likely to be enough to retire on. You simply won’t have enough years of contribution room available. If you don’t intend to retire until age 60 or so, life gets more simple, and you can probably skip this part and just worry about TFSA and RRSP withdrawals.

Quick Capital Gains Review: A capital gain is essentially when you buy an asset at one price, watch as the asset rises in value, and then sell that asset for a higher price. Whatever the difference is between when you bought the [stock, bond, ETF] and when you sold it, that is the value of the capital gain.

It’s important to note that capital gains are NOT taxed until they are “realized” (aka: sold) – even in a non-registered account. Until a capital gain is “locked in” by selling the asset, the rise in value is called an unrealized gain.

Quick Dividends Review: A dividend is basically the money that a company decides to send its shareholders (people who own shares of the company) each year. When you own a share of a company (or the mutual fund or ETF that you own, owns a share of a company) then when the company pays out a dividend, you get sent a cut of that.

When you read about stock market returns over the long-term, the figures that you see are created by adding together the capital gains and dividends paid out of all the companies in that stock market.

Dividends are taxed in a confusing way. This is due to the complicated nature of corporate taxation interacting with your personal taxes. What you need to know about your personal taxes and government benefits is that Canada splits up dividend income into categories:

Dividend Income from Canadian Corporations

When you get paid a Canadian dividend, you have to think about two things:

- The figure that the Canadian Government is going to use when determining your taxable income.

- The actual tax that you will pay, and consequently how much money will go into your pocket.

As crazy as it sounds, these two things are actually quite far removed from each other. In order to figure out your taxable income (which is key for deciding how much cash you get in government benefits such as OAS and the Canadian Child Benefit) the government takes the amount of dividend income that you got paid, and “grosses it up” by 38%.

So if you got paid $1,000 in dividends, your tax filing at the end of the year will declare $1,380 of taxable income.

I know this gross up thing is weird.

It has to do with a concept called tax integration – and it gets tangled up in the corporate taxation world. It’s easier to just accept it as fact and move on.

BUT

Then the Canadian Government and Provincial Governments swoop in and apply dividend tax credits to the situation. How this is done includes a bunch more math, but the end result is that if your taxable income for the year is $50,000 or less, you can actually get money back on your taxes!

Alternatively, if you say, live in Ontario, and are in the highest possible tax bracket, you’d pay a marginal tax rate of close to 40%. Of course, if you’re earning more than $220,000 in taxable income in retirement, then you’re doing pretty all right!

Note: There is a further layer of complication to Canadian-based dividend taxation that doesn’t affect most Canadian investors. If you receive dividends from a Canadian corporation that is not on a stock exchange, you might be receiving what are called non-eligible dividends.

As the name implies, they are not eligible for the Canadian Dividend Tax Credit. For now, let’s put these to the side, as they aren’t really relevant to folks who invest in Canada’s large publicly-traded companies. If you own shares of a smaller Canadian Controlled Private Corporation (CCPC) then some specialist reading is in order.

Dividend Income from Non-Canadian Corporations

When you receive dividend income in a non-registered account, from companies based outside of Canada, those dividends are taxed at 100% of your normal tax rate.

It is as if you earned that money at a job.

There is no gross up or dividend tax credit to consider.

On top of the Canadian tax, many countries also apply a withholding tax to your dividend cash before it leaves their country (usually between 15-25%) – although there is often an offsetting tax credit on this amount to prevent what investors call “double taxation”. All this to say, that it is almost always a good idea to leave your foreign stocks inside of a RRSP and/or TFSA when possible.

Quick Interest Review: When you invest your money in a GIC, bonds, or leave it in a high interest savings account, the money that you will receive back in addition to your original principle is called interest. It is taxed at 100% of your normal tax rate (unlike capital gains and dividends) and is basically as if you earned money at a job.

The table below illustrates how much you’d have to withdraw from a non-registered account, in order to put $35,000 of cash in your pocket. Keep in mind this table is for a single person, and not a couple.

The table below illustrates how much you’d have to withdraw from a non-registered account, in order to put $35,000 of cash in your pocket. Keep in mind this table is for a single person, and not a couple.

Type of Income | Amount That You have to Withdraw to put $40,000 After-Tax In your Pocket | Taxable Income Used to Determine Government Benefits | Effective Tax Paid If You Live In Ontario and Stay Under $49,000 for the Year |

Interest (GICs, High Interest Savings Accounts, Bonds) | $45,758 | $45,758 | (Combined Fed/Ontario rate = 14.40%) $5,758 |

Dividends from Canadian Companies | $40,000 | $55,200 | (Combined Fed/Ontario Taxes owed after Dividend Gross Up = $0) |

Dividends from Foreign Countries | $45,758 | $45,758 | (Combined Fed/Ontario rate = 14.40%) $5,758 |

Capital Gains from Selling Stocks/ETFs for more than you bought them for | $40,710 | $20,355 | (Combined Fed/Ontario rate = 1.75%) $710 |

Selling Stocks/ETFs and Getting Your Initial Money Back | $40,000 | $0 | $0 |

An important thing to note after looking at this chart, is that rarely will you ever be withdrawing ALL of the income needed for the upcoming year from one particular type of income – and that all of that income would be coming from your non-registered investing account.

You’re much more likely to piece together a little from Canadian dividends, some from foreign-based dividends, a little from freelance labour, perhaps a pension, and then maybe some TFSA- and RRSP/RRIF-originating income as well.

Here’s what a more practical tax situation might look like for the average Canadian retiree. I’m using Ontario tax rates because Ontarians make up 40% of the country, and because Ontario’s tax rates are pretty average.

In this scenario, we’re saving their TFSA for later, so not taking withdrawals from there just yet.

- $17,000 from combined OAS and CPP

- $15,000 from a defined benefit pension plan (or part-time work)

- $15,000 withdrawal from their RRIF

- $3,000 from Canadian dividends in their non-registered account

- $4,000 in capital gains from selling stocks in their non-registered account

- $5,500 from the initial money they used to buy stocks in non-registered account

- $500 in interest from their high interest savings account

In this scenario, Doris (our “average retiree”) would owe $6,065 in combined federal and provincial income taxes and does not have to worry about the OAS clawback. The $5,500 that she got back from selling stocks in their non-registered account is not taxable income, but all of the other investment returns and RRIF withdrawals have at least some taxes owing. The effective average tax rate she’ll pay is about 12%.

This 12% average tax rate fits with what I’ve seen as a general rule of thumb for couples in retirement with a combined income of around $80,000. Various tax credits and income splitting opportunities usually result in a lower average tax rate than I think most people would estimate.

Ok – I know that was a lot of reading just to snag the “low-hanging fruit” of withdrawing your retirement income, but if you want to understand how to keep as much of your nest egg in your own pocket as possible – while maximizing your government benefits – then knowing the different ways income is taxed is essential.

Knowing how different types of investment income get taxed will influence what investments you keep inside of a TFSA, RRSP, and in a non-registered account. It will also impact the order in which you withdraw cash from all of those accounts.

Canadian Taxable Income Meets Canadian Government Benefits

Who doesn’t like “Free Money” from the government?

In order to understand the total impact of withdrawing investments from your various accounts, one has to take into account not only taxes, but also the effect those withdrawals will have on their monthly government cheque.

The main government benefits of interest to 55+ retirees are likely to be Old Age Security and the Guaranteed Income Supplement. It’s important to note that your Canadian Pension Plan (CPP) payments are NOT based on taxable income and won’t be affected by your withdrawal decisions. Here’s the two taxable income levels that you have to be aware of:

- After roughly $95,000 every dollar of taxable income that you earn from some retirement side-gigs, withdrawals from RRSPs, pension income, or non-registered investment account income generates a $0.15 tax on your OAS.

- The government has allowed seniors to earn $5,000 of taxable income and still receive their full GIS. However, if they go over that mark, their GIS will be reduced by $0.50 for every dollar they earn. (A steep tax penalty!)

If you want a super creative strategy for maximizing GIS payments while living a relatively frugal retirement check out this chat with pension maestro Ed Rempel. Dividend income and the gross up for tax purposes will not be your friend if you’re trying to maximize GIS payments.

Now if you or your partner are making more than $95,000 after tax in retirement (then first of all – congrats!) remember that you can use pension splitting to keep your income as close to equal as possible, and thus make sure that you don’t pay more of the OAS clawback than you have to.

The different ways to split RRSP and RRIF withdrawals get a bit complicated, but there are almost always strategies available to most Canadians to even out the income between spouses to a large degree.

There are also some creative OAS strategies for folks in higher income tax brackets that involve postponing OAS payments in order to withdraw RRSP income sooner rather than later, and then having a higher “OAS ceiling” when it comes to getting at least some of your government benefits.

A lot of experts recommend postponing your OAS and/or CPP, while drawing down some of the investments in your RRSP and non-registered account a little earlier in retirement. This will definitely be the most tax efficient way of doing things if you live past the age of 83-86.

The tradeoff here is that it’s possible that you withdraw much of your assets, intending to use the government benefits later on, only to pass away before you can make full use of them (and not leaving your inheritance with assets that they could have benefited from).

At the end of the day, I lean toward spending some of your RRSP sooner rather than later, and then relying on the security of your TFSA, CPP and OAS in your later years. If you planned on willing RRSP assets to loved ones, they’re going to get hit with a huge tax bill on those anyway.

Some pessimistic critics will shout that those government benefits could disappear, but no serious expert who I’ve talked to thinks that will be the case.

The CPP is in great shape, and while the OAS is the more likely candidate to get tinkered with at the edges, look what happened as soon as the Harper Government made relatively small changes – they were immediately reduced due to political pressure. I don’t see this changing anytime soon.

The Canadian Child Benefit Clawback for Early Retirees

I’m not sure that it meant to do so, but when the Canadian government created the Canadian Child Benefit, it really gave an incentive to parents who were considering early retirement, or early-partial retirement, to pull the trigger.

Many young parents are not in the retirement mindset, but if you’ve caught “FIRE” (Financial Independence & Retire Early) then perhaps your biggest concern is maximizing your Canadian Child Benefit cheque each month.

You can read on to see exactly how Kornel factors this into his planning, but the basic idea is that you want to keep your taxable income as a household below $37,487 if possible, and after $81,222 the clawback starts to get substantially more aggressive. Note that the CCB works on household income, not personal income.

Again, these are strategies that appeal to people who really treasure the freedom of early retirement. Obviously there are tradeoffs involved with making ends meet with a taxable income of $81,000 when raising a family in Canada. You can use this handy CCB Calculator to play around with the numbers for your specific family.

Depending on how old your children are, and how big a brood we are talking about, this benefit can be nearly $30,000! If your household taxable income gets above about $150,000 though, you won’t be getting much benefit. Scroll down to see how Kornel makes the CCB work to his benefit.

For more details on the CCB clawback discussion, check out this extensive video by Ed Rempel and I, where we discuss why parents with a few children are actually the most highly taxed folks in Canada!

Asset Allocation = How Much Stocks and Bonds Should I Have In Retirement?

Another common question that we get asked is, “As I approach – and then enter into – retirement, what should my overall portfolio look like.”

Like any good personal finance geek, I try to immediately evade these types of questions with: “It Depends”.

But it truly does depend on many variables that will be unique to you. Considerations such as:

- Do you have pension?

- Do you have a spouse to income split with?

- What are your income needs in retirement?

- What is your appetite for risk?

- Do you have a thorough understanding of what investment risk does to your nerves?

- Do you prioritize travelling while retiring young, or leaving behind a generous inheritance?

The answers to any of these questions can drastically change what your asset allocation should look like in retirement. Please check out our retirement withdrawal rates article to understand some general rules of thumb about how to approach asset allocation in retirement.

Generally speaking, I believe that tilting your portfolio more aggressively toward stocks/equities throughout your retirement is probably in most folks’ best interest from a purely mathematical perspective.

This is especially true if you’re fortunate enough to have a personal workplace pension to fall back on. All of that said, thoroughly understanding stock market return risk and how much you should be withdrawing every year are essential to planning your portfolio allocation.

Kornel and I always recommend double checking your preferred strategy with a fee-only financial advisor.

What Investments Should I Keep In a TFSA, RRSP, and Non-Registered Account for Maximum Tax Efficiency?

Now we get into the sprinkles on top of your retirement ice cream sundae.

You can see exactly how Kornel has organized every single one of his investment accounts, and how he withdraws the cash he needs into a high-interest savings account, by scrolling down to his case study.

That said, before your eyes glaze over, remember that Kornel and I like to nerd out about this stuff.

If we can save a hundred bucks by reading for a few hours and getting our arms around concepts such as withholding taxes on US-based ETFs – then that’s what we’ll do.

It’s entirely possible that this particular juice is just not worth the squeeze for you.

Here’s sort of the big picture, and how I’d prioritize “how to put what, where” when it comes to growing your investment portfolio and preparing it for retirement.

1) First things first – maximize any employer retirement incentives. Ideally, try to get your employer to offer some sort of index-based investment option, but if worst comes to worst, go with the mutual funds despite the MER if it means snagging a 50-100% employer match. This is free money.

Now – get that money out of the mutual funds and into index investments as soon as your plan allows you to do so!

2) Decide on your overall asset allocation (see above). This is not an easy decision. Determining your comfort with stock market risk vs fixed income investments is unique to each person, and shouldn’t be skipped over. This is especially true the further we get from the last time investors felt really heavy stress from a stock market drop.

3) Put some money in both your TFSA and RRSP until your TFSA is filled, then fill your RRSP. There are many arguments between what to contribute to first and why. If you earn higher-than-average income (more than 75K) go with the RRSP. If you make below $48K annually go with a TFSA, and if you’re somewhere in the middle split it and don’t sweat the small stuff.

4) After you have decided how much of your investment portfolio you want invested in equities (stocks) and fixed income (bonds & high interest savings accounts), then you want to select your actual investments. Please see our article on Canada’s all in one ETFs, as well as our Questrade vs Wealthsimple article for more information on exactly how Kornel and I personally invest (as well as pretty much every single financial writer that I know).

STOP – Many people can stop here, ignore points 5-9, and jump right to Kornel’s case study. If you start to become overloaded with acronyms & small percentages, then you need to understand one thing:

Don’t let your lack of understanding of the sprinkles stop you from getting started on your retirement sundae!!! Most Canadian investors are better off ignoring the small improvements below if it means that they get started today!

You can absolutely ignore this sprinkle on your sundae, select an all-in-one ETF, buy that one ETF across your TFSA, RRSP, and non-registered accounts – and be JUST FINE!

5) The next level of maximizing your returns involves splitting up your ETFs or robo advisor-managed assets into the non-registered, TFSA, or RRSP accounts where they will receive the least amount of tax penalty.

The two keys to this level of organization are:

- Understanding how income generated from this type of investment gets taxed when it’s outside of your RRSP or TFSA.

- Understanding how countries outside of Canada tax the dividend returns on your stock investments before they land in your pocket.

The basic idea is that foreign governments want another bite of your investment money before it leaves their country. So when the foreign-based companies that you own shares of pay out dividends, these foreign governments generally want a 15% taste of that money before it gets to your Canadian brokerage account. It’s important to remember that this 15% “extra tax” is ONLY ON DIVIDENDS and NOT the overall returns of these stocks.

That said, Canada has a special agreement with the USA when it comes to owning US stocks/ETFs in our RRSPs (but no agreement exists for TFSAs – so definitely DO NOT put US ETFs in your TFSA).

So… here’s a quick look at how various types of ETFs will incur the foreign withholding tax. Thanks to Dan Bortolotti over at PWL for his help on sorting this part out!

Type of Income | Real amount of withholding tax hit when held inside an RRSP on a stock/ETF that gains 6% in capital gains, and 2% in dividends | Real amount of withholding tax assessed when held outside an RRSP on a stock/ETF that gains 6% in capital gains, and 2% in dividends |

Individual Canadian Stocks | N/A | N/A |

Canadian-stock only ETFs (like VCN) | N/A | N/A |

USA ETFs purchased on the New York Stock Exchange in USD (only USA stocks) (like VTI) | Withholding tax does not apply | .3% – Applies, but can be recovered when you file taxes |

US-based ETFs purchased on the Toronto Stock Exchange in CAD (like VUN) | Withholding tax applies – .3% | .3% – Applies, but can be recovered when you file taxes |

International/All-in-one ETFs that hold stocks from all over the world and automatically rebalance – and are sold on the Toronto Stock Exchange in CAD (like VEQT) | Withholding taxes applies – .22% | .22% applies, but you can get almost all of it back when you file taxes |

Fixed Income (Bonds, Bonds ETFs, etc.) | No dividends to worry about | No dividends to worry about |

Horizons swap-based ETFs that seek to turn dividends into capital gains | No dividends to worry about – BUT Canadian legislation is seeking to take away this tax advantage in the near future | No dividends to worry about – BUT Canadian legislation is seeking to take away this tax advantage in the near future |

So, you can tell from the chart above, that generally speaking, for maximum withholding tax efficiency, it makes sense to hold your US-based ETFs in an RRSP, and in USD.

BUT!!!

Of course there is a “but”…

The “BUT!” here is that in order to hold that US-based ETF you’re going to have to convert your Canadian Dollars to USD in order to buy the ETFs, and then back again when you want to spend the fruits of your investment’s labour. PLUS – there are some really smart people who worry about inheritance issues if a person passes away while holding a US-based ETF in any type of account.

You can read Kornel’s case study if you want an example of someone who has optimized to this level and who can explain more about Norbert’s Gambit – the most efficient way to convert your CAD-to-USD.

ALSO – See our article on the semi-exotic Horizons Swap-based ETF products for the ultimate in withdrawal tax avoidance when it comes to your non-registered portfolio.

6) Generally speaking, unless bond returns suddenly shoot the roof, it makes sense to keep your fixed income in CAD funds, and outside of your TFSA and RRSP. There is a math breakdown on this that involves understanding that your fixed income gets taxed at 100% of your marginal tax rate whereas, capital gains and dividend income generally enjoy lower tax rates, but all things being equal, the higher overall returns of equities means that for the most part, it makes more sense to have your equities shielded behind that protecting tax wall of the TFSA or RRSP.

It might be worth noting that some people disagree with me on this since the tax rate on Canadian-generated dividends held outside of a registered account is substantially lower than that of fixed income. You will have to run the math for your specific income level to determine what’s right for you. Personally, I don’t ever intend to have much of my portfolio in fixed income products, as I detailed in our withdrawal rate article.

7) If you plan on residing outside of Canada when you retire, then we have to have a different conversation about what currency you hold your investments in. Generally speaking, it makes sense to hold the majority of your investments in the currency your expenses will be in, if possible.

8) If you want to get really creative, and are confident in your DIY investment skills, check out our Ultimate Guide to the Smith Manoeuver.

Can I Use a Robo Advisor to Make Investments and Retirement Withdrawals Easier?

Yes!

The vast majority of Canadians that want some help with their investments right now are paying tens of thousands of dollars every year, for a level of advice that they don’t know how to quantify. The advice could be good or terrible – they’ll never know – and they’re paying an insane amount for it, regardless.

It’s basically the situation I hope to avoid when I pray to the gods of vehicle repairs!

Canada’s robo advisors (see our Wealthsimple vs Questrade article for more on how to choose the best option for you) charge a fee that is 75% less than what a traditional mutual fund would cost you.

Essentially, what you’re sacrificing when you go with a robo advisor, is the minute control over things like getting those extra couple of withdrawal tax-avoidance sprinkles on your sundae. What you’re getting in return is an excellent index investment strategy, absolute peak ease-of-use (probably the biggest factor for most of us), and day-to-day advice through phone, email, or online chat (just not in person) when needed.

There seems to be a bit of a pervasive myth out there that robo advisors are only for building assets and that you should remove your assets once you’re ready to start spending your nest egg instead of building it. This ignores the reality that we outlined in our retirement withdrawal rate article: that your nest egg is much more likely to grow in retirement than shrink – if you do it right!

Also, with Wealthsimple now becoming more and more like a full service bank with Wealthsimple Cash accounts, a person can easily handle all of their retirement income needs through the Wealthsimple ecosystem.

If you want to dive into the minutia of investing in order to get that last 5-10% of efficiency, then opening a discount brokerage account and going full DIY is your best option. Most Canadians that I know though, value simplicity, and robo advisors really, really help with that at any stage of our financial lives.

0.4% - 0.5%

$5,000

0.35% - 0.55%

$2,000

No Available Promotion

0.2% - 0.5%

None

0.20% - 0.28%

$1,000

No Available Promotion

0.35% - 0.60%

$1,000 For Canadian Residents

0.40% - 0.70%

$5,000

No Available Promo

0.50%

$100 - $1,500

No Available Promotion

0.35% - 0.50%

$1,000

No Available Promo

Flat rate tiered fees: $5-$150

None

No Available Promo

Withdrawing from Your TFSA, RRSP, or Non-Registered Accounts: What’s The Order?!

You’ve done well, Worker Ant.

Whether you’re retiring at 35 or 55+, you have stored up a nice surplus to ensure that you never have to worry about collecting food again!

Choosing what accounts to withdraw money from first, and which ones to leave – all while keeping your asset allocation intact – is really about understanding tradeoffs.

There is no way to tell in advance if the US-based stocks in your RRSP are going to have great compounding returns, or what your age will be when you go to that great tax haven in the sky.

If we knew variables like that in advance, we could create a one-size-fits-all spreadsheet. Instead what we’re going to do is give you a few rules of thumb to apply to your situation – as well as leave you with Kornel’s in-depth case study about how and why he withdraws his money in a very specific way.

- Develop a plan for your 4% withdrawal rate, and correspondingly, how much you will spend in retirement. This will allow you to determine how much investments you will “cash in” to pay for your daily spending needs.

- Remember that factoring in taxation and government benefits should NOT tempt you to get away from your target asset allocation. I know that managing all of these investments across 4-6 accounts for a couple can be tricky – but don’t let a few percentage points on a withdrawal tax rate channel you into an investment strategy that is too risky for your investor profile.

- Spend dividends in your non-registered portfolio first!

- Develop a plan around which government benefits you want to preserve from being clawed back, and what taxation levels you want to be aware of when it comes to your personal income needs.

- After age 55, defined benefit pension income can be split between spouses, and after 65, that expands to include RRIF income as well. Make full use of this tax split. Any fee-only financial planner worth their salt should be able to do this for you, no sweat.

- Decide what you want to do in terms of smoothing your income in regards to deciding when to take OAS and CPP. If you are in great health, there is a strong argument to be made for postponing your OAS and CPP and using some RRSP cash sooner rather than later. Just understand that at 71 years of age you will be forced to convert that RRSP into an RRIF and begin drawing it down. It’s also worth noting the vast majority of folks spend more money in their early “active” retirement, than in their later years.

- Kornel and I both agree that most early retirees underestimate the amount of income they’re likely to produce from hobbies or side gigs that they pick up after their regular 9-to-5 grind is finished. The same principle holds true for retirees of any age.

If you read our 4% withdrawal article, and determined that you and your partner need to produce $60,000 per year of income going forward, then you’d need a portfolio of roughly $1.5M in order to fairly-safely generate that income. However, if you each earned $10,000 per year doing some freelance work or taking the odd casual shift somewhere (maybe after your first year of complete freedom?) then your portfolio only needs to generate $40,000 per year.

As more and more retirees of all ages enter into retirement with larger TFSA portfolios, how you handle the drawdown of this account specifically is going to become vitally important due to the fact that money withdrawn out of a TFSA is NOT taxable income.

This means that as part of a plan to avoid having your government benefits clawed back, it is absolutely essential. It’s also why more and more advisors are recommending maxing out your TFSA ahead of your RRSP for many middle-class Canadians – HOWEVER – keep in mind that the government could change these TFSA rules at any time.

A Real-Life Canadian Retirement Withdrawal Case Study: Kornel Szrejber

Background: Kornel and his wife hit their financial independence number at the age of 32 and 31 here in Canada. When this happened, his wife became a full-time stay-at-home mom while Kornel experimented with different financial independence lifestyles including doing a full retirement, working part-time for an employer, and working for himself on different passion projects.

He currently runs his own financial planning and investing podcast, as well as the Canadian Financial Summit where he interviews the top financial experts across Canada in an effort to increase financial literacy for Canadians. He and his family primarily live off their investments while in their mid-30s, so I thought it would be great to have him as a real-life case study on how he actually does it.

When it comes to withdrawing from your investment portfolio, there are two goals that I aim for.

- Pay no tax (or very little tax) on the amount that I withdraw for day-to-day spending.

- The second goal is to mitigate any clawbacks that can occur if your taxable income for the year is too high. Specifically, if you are retiring around the traditional age, then you want to keep your taxable income low enough to get the maximum Old Age Security (OAS) and maybe even the Guaranteed Income Supplement (GIS), if you can get your income really low.

If you are an early retiree and have kids, then one of your concerns in this department is limiting the clawbacks that you get on your Canada Child Benefit (CCB).

If you are an early retiree and don’t have kids, then you typically aren’t receiving any additional income from the government. In this case, your primary focus is on keeping your taxable income as low as possible so that you remain in the lowest possible tax bracket.

To summarize, you want to withdraw from your different accounts in such a way that your taxable income stays below certain thresholds (whether that’s below a certain tax bracket, or below an amount where clawbacks on your benefits begin).

Here Is How I Withdraw From My RRSP and TFSA Accounts

Before we dive into the details, keep in mind that to fully tax-optimize this process, it can get pretty complicated.

Before pulling the retirement trigger, I definitely recommend seeking the advice of a good fee-for-service financial planner and a good tax accountant to make sure that you didn’t overlook anything. That’s definitely what we did, even though I already specialize in this field.

There’s no room for ego here, as the stakes are too high. Therefore, no matter how much of an expert you are, I still suggest you pay the money to get a good financial planner and accountant on your team for a second opinion. This field is complicated with lots of nuances, and nobody knows every single strategy out there, and you really do want a plan and process that is custom-tailored for your specific situation.

Withdrawing Dividends and Interest Investment Income

When it comes to living off your portfolio, the income will come from dividends, interest, and from selling off some of your investments (capital gains).

First, let’s focus on the dividends and interest that is received in our different investment accounts.

After that, we’ll talk about generating more income by selling off some of our investments.

Withdrawing Dividends and Interest Outside of Your RRSP and TFSA

In our taxable accounts, the ETFs that we hold pay dividends. These arrive automatically and are deposited into our Questrade Account as cash. [See our Questrade vs Qtrade article for more on our favourite broker platforms.] These can then be withdrawn easily and spent.

At the end of the year, Questrade will send you tax documents that indicate how much you received, and you have to include that when doing your taxes.

In taxable accounts, we hold a lot of XIC. This is the ETF that tracks the Canadian market (the S&P/TSX). The reason that we chose to hold the Canadian index in our taxable accounts, is due to the dividend tax credit that is received when holding Canadian dividend payers in this account.

We still hold some US and international ETFs in our taxable account, but the emphasis is definitely on Canadian dividend-paying investments since under the right conditions (primarily lower-income levels), you can actually receive those dividends tax-free.

International and US dividends, on the other hand, are taxed as regular income and so they are nowhere near as tax efficient as holding a Canadian index ETF in this account.

Best 2026 Broker Promo

Up To $2,000 Cash Back + Unlimited Free Trades

Open an account with Qtrade and get the best broker promo in Canada: $100 when you invest $1,000!

The offer is time limited - get it by clicking below.

Must deposit/transfer at least $1,000 in assets within 60 days. Applies to new clients who open a new Qtrade account by July 31, 2026. Qtrade promo 2026: CLICK FOR MORE DETAILS.

Withdrawing Dividends and Interest in RRSP Accounts

In our RRSP accounts, we only hold the US market, using the ETF VTI.

Our main reason for this is that due to a tax treaty between the US and Canada, US dividends are exempt from US withholding tax when held in an RRSP.

The challenge with holding something like VTI for us Canadians however, is that it can only be bought in US currency (if you instead buy something like VUN which is the Canadian equivalent in Canadian currency, you won’t get that withholding tax benefit).

Therefore, we used a technique called Norbert’s Gambit to switch our Canadian dollars to US currency in our RRSP. We then used that US currency to buy VTI.

WARNING: If you are also going to buy VTI in your RRSP for this tax advantage, make sure that you do actually use Norbert’s Gambit for the currency conversion. If instead you just let your brokerage buy the currency for you, then you will likely be charged a LOT more, making the withholding tax advantage a lot smaller, due to the heavy fees that you’re paying for the currency conversion.

When dividends are issued in our RRSP, we can’t just take them out and spend them because:

- They are in US currency

- A portion of the withdraw will be withheld to pay for Canadian taxes (which you can get back later if your tax rate is low enough)

- Questrade will charge you an additional fee of $50 to $100 when you take money out of your RRSP without using a RRIF. If you are taking out your RRSP dividends every quarter, then that means at least an additional $200 per year in unnecessary transaction fees.

Because of this, I have instead been doing a simple ETF swap to withdraw those dividends. Here is the process for you:

Withdrawing RRSP Investments By Swapping ETFs

- First, I take the RRSP dividends that were paid out from VTI, and I invest them to buy more VTI in my RRSP. This way, I don’t have to deal with any of the three issues mentioned above.

- I also take that dividend payout amount from step 1 which is currently in US currency, and I check how much that would be if swapped it for Canadian currency.

For example, if the dividend payout was $1,000 USD, I just use an online conversion tool like xe.com to get an approximate amount of how much that would be in Canadian dollars. In this example, that would be around $1,304 CDN.

- Next, I sell a comparable US ETF that I also have in my taxable accounts which is in Canadian currency. In this example, I would sell off $1,304 (from our example above) of VUN (which is the Canadian version of VTI that is in Canadian currency).

It sounds a bit complicated, but by doing it this way, I can withdraw dividends from my RRSP using my taxable account, and not be faced with the 3 issues mentioned earlier.

There is also a tax advantage of doing this since if I withdrew the money directly from my RRSP, it would be taxed as regular income. However, since I am just selling the Canadian version of that US ETF, I am instead incurring capital gains which are taxed much more favourably than regular income.

The Long-Term Repercussions

After doing such swaps longer term, there will one day come a day when I no longer have any US ETFs left to sell outside my RRSP.

At this point I’ll have to decide:

- Do I keep reinvesting the US dividends in the RRSP? This is not a bad option but of course, it also means that there is less spending money coming in every 3 months for day-to-day living expenses.

- Do I begin actually withdrawing those dividends from the RRSP? This is fine too but you wouldn’t want to do it every quarter when dividends are issued, due to the transaction costs of currency exchange and the fees associated with moving your funds from an RRSP to a chequing account (i.e. the “plan deregistration fees”).

Because of these fees, I would just do the RRSP withdrawal transaction once a year where I withdraw 1 year worth of dividends AND any other money that I want to take out of my RRSP to live from (by selling off some of our RRSP investments).

In this scenario, since we are now withdrawing from our RRSP, we need to factor those withdrawals into our income to make sure that we don’t accidentally step into a higher tax bracket (or experience a major clawback on our government benefits).

You can also consider setting up a RRIF at this point, to avoid having to deal with the withholding taxes when withdrawing directly from your RRSP, and to avoid having to deal with the “plan deregistration” fees.

The reason we haven’t done a RRIF yet is that with a RRIF you have to withdraw a certain minimum amount from your RRSP every year. For tax efficiency purposes, I don’t want to be forced to withdraw anything from my RRSP yet, and so for now we are not using a RRIF in our early retirement.

In particular, since we are generating some side income in our retirement through my investing and financial planner podcast and the Canadian Financial Summit, I never know exactly how much extra income I’ll receive from these two bonus sources of income throughout the year.

Therefore, if we have a good year in either of those side businesses, I don’t want to be forced to withdraw from my RRSP using a RRIF because that could make us jump to the next tax bracket, or heavily increase the amount of clawbacks we receive.

This is an important consideration because while early retirement and never having to work again sounds great in theory, the reality is that almost every single early retiree still ends up earning some sort of side income, working on projects that they love, where the money is no longer the primary motivator.

If you research the FIRE movement and those that have actually pulled it off, you’ll notice that almost everyone has quit their regular day job, and now just found a way to monetize their passion projects. That’s definitely what I did too.

So, the bottom line here is that you really should assume some level of side income when you are financially independent or “retired”. This will let you quit your job earlier but will also impact your taxes and withdrawal strategy, so make sure to factor that in when doing your plans to mostly live off your investment portfolio.

Withdrawing Dividends and Interest in TFSA Accounts

Dividend and interest payments that occur in a TFSA are tax-free.

Because of this, we never keep any bonds in this account as those tend to have much smaller returns than stocks.

The logic for this is that you want assets that are going to return the most in your TFSA, as this is the only account where you can harvest those dividends and growth tax free.

In other words, since you have a finite amount of TFSA room, you want to put the highest growth assets in there as that way you are shielding as much growth as possible from tax.

Our dividends arrive as cash in the TFSA account every three months. When this happens, I move the cash out of the TFSA and into my bank account, ready for spending.

Unlike an RRSP, you do get your contribution room back every year with a TFSA. Therefore, in January – when we receive the new TFSA contribution room – I move the correct amount of investments from our taxable account into the TFSA to fill up the new contribution room (currently that’s $7,000 per person) plus the dividend amount that I took out in the previous year.

Another option:

A different approach is to instead reinvest those dividends in the TFSA, and then just sell-off that exact amount in your taxable account (using the same ETF).

This way, your TFSA is 100% maxed out the entire time allowing you to maximize your tax-free growth.

The reasoning here is that if you withdraw those dividends from the TFSA, then you no longer have that withdrawn money in your account growing tax-free.

What investments do I put into my TFSA?

Since Canadian index ETFs are better for taxable accounts (due to the dividend tax credit), and since the US index is more tax efficient when it’s in your RRSP (due to being exempt from the US withholding taxes), it makes sense to have a large portion of your TFSA be filled with international index ETFs like XEF.

Once again, since we only want the highest growth investments in here, we don’t put bonds in the TFSA.

Withdrawing Capital Gains from RRSP and TFSA Accounts

Now that we have our dividend money ready for spending, the next step is to sell off a portion of our investments to meet the rest of our spending needs.

Of course, we can’t withdraw too much or we risk running out of money in our retirement. This is why we need to ensure that we don’t exceed our safe withdrawal rate.

To give you a real-life example, we’ve currently settled on a 4% variable withdrawal strategy Kyle writes above in that safe withdrawal article linked to above. In addition to that, I also have enough of a fixed income cushion so that we can wait 4 years for the markets to recover without having to sell any of our equities.

This way, even when we have another financial crisis like what happened in 2008, we wouldn’t be forced to sell any of our equity holdings at a loss (since we can just use the fixed income cushion while waiting for the markets to recover).

In other words, we use a 4% variable withdrawal when markets are good. When they are bad however, I sleep well at night knowing that I can wait 4 years before having to sell any of our equities. Here’s a chart Kyle made for our average stock market returns in Canada article which shows why I use four years as my “safety net” assumption.

Of course, there are no guarantees, but you also don’t want to end up too conservative as that comes with its own set of issues (such as inflation and missing out on capital gains). This portfolio allocation works well for me, but definitely isn’t the ONLY way to set up your portfolio for retirement.

Anyway, let’s use a $1,000,000 portfolio as a base for this example.

Dividends bring in a bit over 2% yield, generating a bit over $20,000 a year. This leaves us with another $20,000 that we want to withdraw by selling off some of our ETFs.

Keep in mind that here we are assuming that the markets had a good year and so we have no need to dig into our fixed-income cushion. Instead, we are simply harvesting some of our gains, and not digging into our principal at all.

So, the question becomes, where do we take the $20,000 out from? Do we withdraw from our TFSA, RRSP or taxable account?

This is an important question as you are taxed differently, depending on which account you withdraw the money from.

The first thing to remember is that the lowest federal tax bracket is if your income is below $58,523 per person in 2026 (and now enjoying a lower 14% tax rate as well).

(Don’t forget there are provincial tax brackets to consider as well. They range from about $30,000 in Nova Scotia to $60,000 in Alberta. Ontario and Quebec are about $53,000.)

The strategy is therefore that you want to withdraw from the different account types (TFSA, RRSP, Taxable) in such a way that neither you nor your partner ever exceeds that lowest tax bracket of about $58,000.

If you are receiving government benefits like the Canada Child Benefit (CCB), OAS, or GIS, then each of those also have certain income levels at which the clawbacks start. In this case, you also want to extract your money in such a way so that you ideally never hit the clawback number (this way you get the full benefits).

For example, the clawback for CCB starts at a household income of $37,487. Therefore, you want to withdraw from your accounts in such a way that you ideally stay below $37,487 in household income. If this is not possible because you want more spending money, then you still want to minimize the amount that you go over this $37,487 clawback threshold as the more income you take out, the more your benefits will be clawed back. Remember though, that you can each withdraw that amount.

Selecting anyone off of our Best Financial Advisors in Canada list, and they will be able to use their software to help you optimize for this.

In a Nutshell:

Any money that you withdraw from the RRSP will be counted as regular income. Therefore, every dollar that you take out from the RRSP will directly apply towards your $58,000 lowest tax bracket.

Any money that you withdraw from your TFSA will not contribute at all to your income. Unfortunately, you only have a limited amount in your TFSA so you can’t just live mostly from your TFSA long term.

Lastly, in your taxable accounts, when you sell off investments, the amount that you are taxed is determined using your adjusted cost base (ACB). Since capital gains are taxed favourably, a $1 withdrawal doesn’t count as a full $1 addition to your income.

Therefore, when selling off your investments, RRSPs are the least efficient (since they fully add to your income), investments in your taxable accounts are mid-efficient (since they partially count towards your income), and investments in your TFSA are the most efficient as they don’t contribute to your taxable income at all.

Hence, it’s a very delicate balance/dance between how much you withdraw from each account, to hit the exact amount of income that you want to report to the CRA.

For example, if you take out too much from your RRSP then you may jump to the next higher tax bracket and have your government benefits clawed back significantly.

If on the other extreme you just decide to purely live off your TFSA. Then while that is great short-term since you won’t pay any tax, what ends up happening is you’ll deplete your TFSA too fast and won’t be able to use that money as a tool to help keep you in the lowest tax bracket in the future, and to help maximize your government benefits.

Hopefully you aren’t too disappointed that there isn’t some perfect one-size-fits-all solution that is perfectly tax-efficient for everyone, and that every Canadian can follow no matter what their financial and family situation is.

However, I hope the above gave you some insight on how the system functions, and about the tax-saving optimization that can take place. My best advice to you is to use this knowledge to have an intelligent conversation with your fee-only financial planner and tax accountant so that you can have your retirement withdrawals optimized for your spending needs and personal situation.

By knowing this, you can ask them the right questions and make sure that they are covering all your bases to ensure that you are paying as little tax as possible when living off your portfolio.

Ultimately, the difference between having this optimized can easily mean an extra tens of thousands of dollars over the course of your early (or traditional) retirement.

What’s the worst-case scenario in addition to losing all that money?

Well, that would be running out of money in your retirement and having to go back to work.

So while this can be complicated, I’m glad that you’re learning this now so that you can hit your financial goals earlier, and hopefully avoid any catastrophic losses that may be lurking.

I’m interested in what other retirement withdrawal strategies are out there, and what people are doing as the balance practicality of logistics, with tax optimization strategies. Let us know if you think you have a unique take on this topic as we found it really really enlightening to question each other’s assumptions in working through these retirement withdrawal variables!

Withdrawing from a RRSP or TFSA to Fund Early Retirement

When updating this article for 2023 I decided to interview Frugal Trader (FT) on how he manages this tax efficient withdrawal strategy in early retirement. Here’s what he had to say:

So just a quick update FT, what accounts do you and your wife have open currently.

We have the following:

- RRSP x 2

- TFSA x 2

- Non-registered accounts x 2

- Corporate investment account x 1

- Small defined benefit pension accessible at age 60

What is your game plan in regards to withdrawing from your TFSA and RRSP?

Well, generally speaking I like to recommend that Canadians leave their TFSA and RRSP alone as long as possible when they retire in order to make maximum use of the untaxed compounding, but if you leave the RRSP too long, you need to be careful that you don’t leave yourself making RRIF withdrawals that impact your OAS clawback.

Personally, I don’t think we’ll wait until 71 as I intend to leave my TFSA for as long as possible, but want to make sure that I’m not forced to take out income when I don’t want to.

So what is your logistical gamplan as far as withdrawing from your accounts each year in early retirement?

My wife and I might have overplanned or underestimated the stock market when we accumulated our assets. It turns out that we likely could have retired much earlier – or at least taken reduced hours. At this point, we actually don’t really spend any more than the dividends (about $73,000 per year) our portfolio spins off. So we basically just fund our daily living with that.

Here’s what I would recommend for most people though (and what I wrote several years ago):

To fund early retirement, my strategy would be the following:

- Use dividends from non-registered accounts and corporate portfolio first. Using dividends would allow for tax-efficient income, especially for early retirees. This may get to be a challenge when you approach OAS time as dividends are grossed up by 38%. So if you make $40k in taxable eligible dividends, it will look like $55k for income testing against OAS. Something to be mindful of if you are approaching senior status. But being someone with 20+ years until senior status, the tax efficiency of dividends are welcome and realistically, it’s hard to predict old age security benefits 20 years from now.

- Use RRSPs to fund the difference in your budgetary spending. While dividends from with non-registered sources are not quite enough for our expenses (at the moment), I would top-up our income by drawing down the RRSP’s. While it wouldn’t deplete the RRSPs, it would help keep it to a more manageable level when we reach forced RRIF withdrawals age.

- Leave TFSAs intact as long as possible. Combining non-registered accounts and RRSPs for spending will give us a lot of flexibility with the TFSAs. We could keep the TFSAs compounding over the years OR simply spend it. It will likely be a mix of the two. This can potentially be used as a future slush fund for luxuries such as travel, vehicles (likely one vehicle household by that point), and/or to leave to the estate/charity. Thankfully, TFSA withdrawals are not income tested for seniors benefits (as of right now!).

- Delay OAS and/or CPP – With enough income to live on via dividends and drawing down on our RRSPs, we may delay OAS and/or CPP. I know we wrote in-depth about the pros and cons of delaying your OAS and delaying your CPP about a month ago here on MDJ.

Are You Saving Enough for Retirement?

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Try Now With 100% Money Back Guarantee*Data Source: BMO Retirement Survey

Any final tips for Canadian retirement withdrawal strategies?

Definitely remember to make use of income splitting as much as possible in retirement. Once you switch over to a RRIF, or if you have a personal pension, you can use income splitting to make sure that both you and your spouse end up in the lowest possible tax brackets.

This is especially important if one spouse continues to work a little bit, or has substantially more pension income. I’ve also used our corporate account to act in the same way as a income split instrument.

Kyle,

Thank you for this very informative article. If I could just make one point and ask one question. Defined benefit pensions can be split with a spouse at any age, not just after age 55. I think age 55 is often cited because most, not all, DB pensions can only be accessed at that age. The OTPP, for example, can be accessed at age 50 and is eligible for income splitting as soon as you start it. For my question, where Kornel does the ETF swap and takes out the equivalent amount of the US dividend in his RRSP from his non-registered account, why does he base the amount of the withdraw on the dividend payout? Why not set his own amount or percentage? He reinvests the dividend in his RRSP anyway, so it’s not a matter of convenience that the cash is just there ready for him. I hope you understand my question. Thanks again for all your great work!

Kudos on such a nice article. I read it thru thoroughly but my situation is not addressed; so I thought I will pose the question:

I am 82. She is 84. No RRSP; No fixed income (Bonds, GICs) investments; No preferreds. TFSA maxed out and it is in the range of 300K++ each – for the both of our TFSAs. Non-R accounts show phenomenal return due to DRIPS and magic of compounding – only because we both have been investing – with belt tightening – from our early 30’s.We have always been in securities (100%). We have always been DIY investors. No full service brokers and no robo advisors. At present, our cash position is quite comfortable. Zero OAS for both of us – tax man took away this “free” gift. It is fully clawed back. We basically live on CPP + company pensions. We still live frugally without much sacrifice.

Now the question – my income tax is quite high with all those USA + Cdn in NReg accounts. I was searching for answers as to how to reduce what I pay to CRA. I do not know any strategies left open to “old and OLD” people like us. I thought this article will help. It helps me understand certain things better but it addresses mostly early retirees, RRSP holders and RIF withdrawals etc… but not the one like my case. I did not discuss my situation with anyone but if I do I am sure the answer will come back as: “well pay the taxes because you make too much money”.

Can someone throw some light on this situation and show me how to withdraw my non-R. I just started to stop the DRIPS on my Cdn account but my US account is still running on steroid. I am all ears and willing to listen if you can show me a strategy to reduce my taxes. I have a slew of cap gains. I also have cap losses of other years. If I collapse my non-R, cap gains will ding me and then what do I do with all that money that I cashed out? Even after offsetting cap losses, cap gains will be there for CRA to come after me.

We have many kinds of charities that we support where some get our securities at year end and some get cash (even if it does not qualify for tax deduction).

Can you please help how a case like mine can pay less tax? Yes, paying my fair share is entirely legit but I think somewhere I am making mistakes that comes to haunt me every year. The new thing now is I have to pay installments every quarter based on last year’s income.

Hi Bala, to the best of my knowledge, there aren’t a lot of easy wins available to you. If you’re hitting the income splitting wins with your spouse and maxing out your legal tax deduction, there isn’t a lot of manuevering left. Depending on how the Non-Regs are invested, there might be something there in regards in to investing in tax efficient ETFs like the Horizon ones I wrote about on this site. That would delete your dividend income from your tax return – and the gross up that is probably killing your OAS. But, the piper will be paid at some point in the form of capital gains. I’d focus on “income smoothing” at this point with the idea being to stay withing specific tax brackets each year by controlling for capital gains. In your situation, I’d argue that a little bit of long-term planning and tax advice will probably more than cover the cost of an advice-only financial advisor. That’s where I’d start.

I am 80 years old and my daughter is 50 years old – I have $695,343 in my Rif which is so high along with my NR being so high{much higher (living a long time helps) that the income from both withdrawals from Rif and dividends from NR have many years ago made preservation of any OAS impossible (one of my original full service brokers told me that none of her ultra rich clients ever fret over the loss of their OAS). Thus,completely the opposite of what u younger folk are striving for like Mr millionaire) the only possible strategy has been to do so well on the investments that the total amount i earn in capital and income in my Rif never goes down and perhaps goes up not withstanding the minimum Rif withdrawls to ameliorate the taxes when i complete this earthly jouney. I am stuck in this process and the only reason i am telling my different story is just to show another aspect of dealing with the high eventual taxes at least one that is not risky.

As to my daughter she has 30 years more than me with her Rsp and Rif (i am her Trading Authority on Self Directed accounts because her other lives are too busy to do it and we do not want to use expensive managers) to run them. Her Rsp currently at $661,366 – the reason it is so high(not so much right now) is from a previous employer she obtained 409,640 shares (not paying any dividends of that publicly traded comp) @.06 but it has traded as high such that it was over 200k at one point but now $35K. She is of strong-minded that it is a strong candidate for a take-over in the vicinity of at least $1.00 because Its product will be in strong demand once it is completly developed . Her original error was not puting that stock into a NR account 17 years ago when she acquired the shares. So the reason i am telling her story, even tho ive told her fairly recently to stop puting any more contributions into her RSP but to think of early de-funding maybe age 60 when she retires from her current employment to now start puting further investment $ into her cash account which is at zero – following what Millionaire and other sites recommended. However today i am thinking that she has already corssed the tipping point and should do exactly as i am doing forgetting the OAS thing – so called “free money” and get tax delayed gains in RSP. Author of this Article and other knowledgables what do u think? Thks

Let me take a step back in life. I’ll setup a scenario and tell me what you think. You want to leisure work retire early, say 45 where your working income is much lower and than completely stop working at 50. You know this when you’re quite young. You are happy living off a modest income, say below $50k a year. Should you stash your income in RRSPs, TFSA or something else, or a balance. I would think you max out your RRSP contribution each year because you’ll have decades to withdraw it below the ~$45k tax bracket? Presumably your working income is well over $100k.

If your current income is going to be in that much of higher of a tax bracket, I’d say prioritizing the RRSP route makes a lot of sense Julian!

You mention in the article, that you “are assuming that the markets had a good year and so we have no need to dig into our fixed-income cushion. Instead, we are simply harvesting some of our gains, and not digging into our principal at all”

Can you talk about what your cutoff is for a “bad year” where you would did into your fixed income cushion? Obviously the market being down 10% would be a bad year, but what rule do you have in place for making that decision. What would you do with a 1% gain in your investments (excl your fixed income)?

In a good year, what are you doing with the fixed income cushion that has matured? Are you rolling over to the same vehicle but at a longer term (eg 5 year), or are you now looking at different vehicles? Would you ever consider individual bonds versus bond ETFs?

I assume what Kornel was getting at here PJD is that if your spending needs required more than the 4% + inflation baseline, then you would be required to delve into your fixed income cushion. When the fixed income matures, I would want to keep it liquid as I may need that in a hurry if the market goes downwards. Personally, Kornel worries about this more than I do. I think there are some compelling reasons to keep as much of your money in equities as possible, so I’m pretty comfortable keeping 12-18 months of cash in a HISA (very liquid) and just having the rest in equities – especially if I’m finding an early retirement that is like to span 50+ years for at least one of my wife or myself.

But to answer your direct question – it would be whenever the market returned less than you needed to withdraw to fund daily life.

Awesome article. So much info all in one place and we’ll explained. You are helping Canadians. Thank you.

Much appreciated Mark!

This is simply an excellent post Kyle and Kormel…

I have referred back to this info multiple times now. I am in the process of constructing a self-directed portfolio (from scratch) in the hopes to execute a 70/30 ETF allocation post-retirement that would enable me to achieve a desired 3.06% Dividend Yield payout to fund a $40k annual living expenses. If you are able to chime in on my personal situation and offer some insights, I would very much appreciate your guidance and assistance to determine if I understand the blog correctly from a tax-efficiency perspective. Below are the details.

RRSP / LIRA (household contribution room maxed)

XUS.TO – – – 26% – – – $330k~ (R) / $40k~ (L) Semi-Annual Dividend Payout

XEF.TO – – – 10% – – – $140k~ (R) Semi-Annual Dividend Payout

XEC.TO – – – 5% – – – $ 70k~ (R) Semi-Annual Dividend Payout

TFSA (household contribution room maxed)

ZRE.TO – – – 10% – – – $140k~ Monthly Dividend Payout

Non-Reg

XUS.TO – – – 4% – – – $ 50k~ Semi-Annual Dividend Payout

XIU.TO – – – 5% – – – $ 70k~ Quarterly Dividend Payout

VAB.TO – – – 30% – – – $420k~ Monthly Dividend Payout

PDC.TO – – – 10% – – – $140k~ Monthly Dividend Payout

1-RRSP/LIRA

All Dividend withdrawals by ETFs.TO holdings (under RRSP) would be subjected to both US and foreign withholding taxes that will NOT be recoverable at tax time? Also, there is a minimum 10% withholding tax imposed by CRA on any withdrawals that is deemed to be recoverable (assuming that your overall household income is at zero-rated tax level at year-end)? All Dividend withdrawals will be considered as regular income taxed at your marginal rate?

2-TFSA

All Dividend withdrawals under ZRE.TO would be subjected to withholding taxes that will NOT be recoverable at tax time but the Dividend withdrawals are TAX FREE (vs if it was held under Non-Reg, withholding taxes on ZRE.TO is refundable but Dividend withdrawals counts as regular income taxed at marginal rate)? Essentially, I am trying to quantify PROS vs CONS on where the ETF itself is best to hold.

3-Non-Reg

a) All Dividend withdrawals under XUS.TO would be subjected to US withholding taxes but will be recoverable at tax time? It is also counts as regular income taxed at your marginal rate?

b) All Dividend withdrawals by both XIU.TO and PDC.TO would be subjected to withholding taxes but will be recoverable at tax time? They are also classified as Canadian Dividends and will be eligible to claim DTC at tax time?

c) All Dividend withdrawals under VAB.TO would be subjected to withholding taxes but will be recoverable at tax time? It also counts as regular income taxed at your marginal rate?

4. Do you see a much different configuration (than what I have listed above) that you would either consider or proposed to achieve the desired end-result of funding a $40k annual living expenses via 3.06% Dividend Yield payout and having to execute the plan in a very tax-efficient environment? Essentially, based on the selected ETFs, I am wondering if I am even placing them in their proper slots (being RRSP, TFSA, Non-Reg) to achieve the objective?

Hoping that I am not that far off from understanding the significance of your blog and if I am, kindly do offer some comments and feedback for consideration. I look forward to your input. Thanks.

MC

Everyone is different i.e. income, pension(s), savings, age, etc. I am building my retirement income stream plan; in the context of everyone is different, here is mine (at a high level) and still a work in process. Budget/track spend on fixed verses variable costs. It is a cash wedge bucket strategy re-balanced/reviewed yearly. Initially it is a DIY plan, with yearly professional reviews (income planner and accountant). My early retirement ( almost 100% of my fixed costs will be from OAS, CPP, Annuity, and variable will be from RIF. Therefore, everything > 70 is bulletproof income and as variable costs start to drop with age. I currently hold, TFSA (dividends), RRSP 50/50 (VBAL, VCNS), some US dividends, until 71, RIF them and break them apart into Bond/Equities ETFs – so Bonds will feed the GICs year over year (as they mature and moved into cash), and the Equities (bucket 3) will be held for the long game. Each year TFSA will be topped up (again this is not taxable to estate) from RIF and will be held in dividends. Life insurance, TFSA’s and remaining assets should leave a sizable estate.

Many thanks Kyle and Kornel for such a comprehensive and rare article on living off our hard saved investments.

In my retirement spreadsheet, my drawdown plan includes the Federal and Provincial (Manitoba) Pension Income Tax Credits and Age Amount Tax Credits.

As I’ll have some income from a DB work pension, the Income Tax Credits are available at age 55. There are no clawbacks/reduction of these credits. To utilize the credits, you need to ensure that you have some (a few thousand a year) of pension income i.e. a DB at 55+, or RRIF/LIF income at age 65+.

The Age Amount Tax Credits kick in at age 65, but there are clawbacks starting at around $38K Federal and $27K Provincial. By carefully managing the taxable and non-taxable income, and balancing the income between me and my wife, over 12 years my spreadsheet suggests that we’ll achieve a total of $27K (in today’s dollars) of tax savings.

So helpful to have this all summerized. Thanks so much.

No problem Glen! Do us a favour and let us others know about it!