How to Become a Millionaire in Canada

Most of us have wondered what it takes to reach millionaire status in Canada. We certainly don’t advise getting involved in any “get rich quick” schemes, but we do have practical steps to share that you can take to start your journey to become Canada’s next millionaire.

The majority of millionaires in Canada didn’t get rich by winning the lottery or by receiving a large inheritance. With determination and proven wealth-building strategies, working class Canadians like engineers, educators, and nurses reach millionaire status every day.

I am sharing with you the easy-to-implement tips I used to reach financial independence so that you too can join the millionaire club in Canada, and live a rich life.

Best 2026 Broker Promo

Up To $2,000 Cash Back + Unlimited Free Trades

Open an account with Qtrade and get the best broker promo in Canada: $100 when you invest $1,000!

The offer is time limited - get it by clicking below.

Must deposit/transfer at least $1,000 in assets within 60 days. Applies to new clients who open a new Qtrade account by July 31, 2026. Qtrade promo 2026: CLICK FOR MORE DETAILS.

How I Became a Canadian Millionaire

Looking back, at a high level, this is how I became a millionaire before the age of 35:

- I started young with wealth building in mind! Like many young people, we started off with relatively high debt (mortgage, car and student loans). We focused on being as efficient as possible with our money to get rid of that debt.

- Our first house was a 2-unit apartment where we lived in one unit and rented out the other. While it was a little work being a landlord, the rental income offset a large portion of the mortgage payment and we were able to deduct mortgage interest on taxes!). This is an example of “house hacking”. Traditionally this means renting out a suite of your home (as we did), but you could also rent a room to a roommate, on airbnb, or host an international student. I should note that we live in Eastern Canada where real estate prices are (still) fairly reasonable.

- Even as our incomes increased, we kept our lifestyle in check (we still to this day live a fairly conservative lifestyle). This enabled us to increase our cash flow overtime to pay off debt early and build long-term investment portfolios at the same time!

- With our expenses under control, we grew the other side of the equation – income! We purchased another rental property, I worked two jobs, and started an online business that expanded over time. We invested the increased cash flow/savings with the goal of letting the investments compound over the long-term. Doing all these side hustles was great but with a growing family the extra activities had to be scaled back over time.

- When I first started investing in my teens, I went after home run stocks (Nortel anyone?). Over time, I honed my investment strategy to focus on keeping costs low, building a portfolio as diversified as possible (index investing), with a tilt towards generating tax efficient income (dividend investing). To this day, I own Canadian dividend stocks for my Canadian market exposure, and index ETFs for international exposure (with some US dividend stocks thrown into the mix). To give you an idea on what an index portfolio can return, we started an RESP at the height of the market in 2008 and despite this, the portfolio has returned over 8% annually.

- Becoming a millionaire takes time and you are going to want to seek out the best long-term investments. For those of you just dipping your toes into investing you may feel more comfortable looking for the best low risk investments.

- However, if you are going to need to access some of your money in 5 years or less, you will need to wisely invest your money in the short term. You could do this with a Guaranteed Investment Certificate (GIC), a High Interest Savings Account (HISA) or a Cash ETF. There are pros and cons to GICs, HISAs and Cash ETFs, as well as different situations in which you’d choose one over the other.

- Check out this post on more nitty gritty details of my million dollar journey.

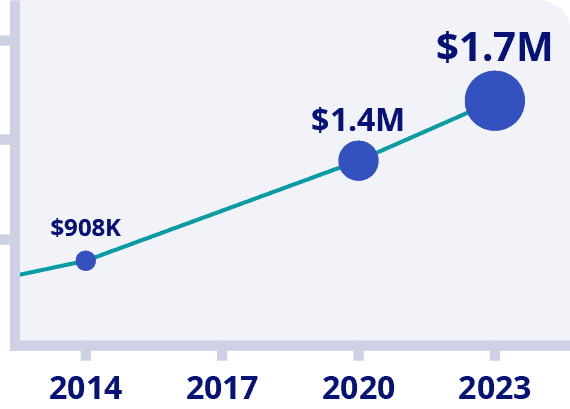

Are You Saving Enough for Retirement?

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Get $50 Discount With Promo Code MDJ50

*100% Money Back Guarantee

*Data Source: BMO Retirement Survey

Tips for Getting Rich in Canada And Making Your First Million

1) Get in the Millionaire Mindset

To get into the millionaire mindset, the first step is to focus on your “why”.

Is your drive to become a millionaire so that you can retire comfortably at a reasonable age?

What about achieving financial freedom in order to give yourself a feeling of financial security without having to worry about having a job solely for the purpose of providing income?

Quantify the amount of wealth you want into an achievable and measurable goal.

An efficient way to work towards your goals is to measure your progress. I used my net worth as my wealth metric over the years.

2) Get your (Bad) Debt Under Control

Believe it or not, there are two types of debt.

Bad debt and good debt. Some may consider all debt as “bad”, so perhaps a better way to look at it is bad debt, and “less-bad” debt.

Bad debt is defined as borrowing to buy a depreciating asset. So that could be a large car loan (cars typically decline about 50% of their value by year 3 or 4) and even worse, with a prolonged loan term. Even so, at least car payment interest rates can be as low as 0%, but there really is no excuse for credit card debt.

Credit card debt typically starts in the 12% to 18% range which can really eat into your cash flow (and derail your plans to get rich) if you let the balance grow enough.

What about “good”, ie. “less-bad” debt? This is generally borrowing to purchase an appreciating asset that pays you (like investment properties and/or equities). This has the double benefit of appreciation over time, and a tax deduction on the interest paid. Note though, borrowing to invest (leveraging) requires high-risk tolerance and should be carefully assessed before taking the leap. Here’s some more information on my leveraged investing strategy using the Smith Manoeuvre.

Some might consider a mortgage on your principal residence “good” debt, but it’s debatable, but it’s definitely “less bad” than a car loan. Get aggressive in paying off bad debt and take your time with good debt.

For those of you with mortgages, here are some tips on how to become mortgage free.

3) Learn to Save

For regular working folk, the easiest way to become rich is to save and invest. At least that’s how we did it.

The first step in that equation is to find a way to save as much of your cash flow as possible. How do you do that? You need to first figure out your cash flow.

Open up those credit card/bank statements and calculate what your regular expenses are over the last 12-month period (longer if you have the data). Then calculate the difference between your income and your expenses. The result is your cash flow.

The goal is to increase your cash flow as much as possible. For people just starting out on this wealth journey, the lowest hanging fruit is becoming more efficient with your expenses.

If you find that your expenses need to be reigned in a bit, there is hope! Here is a list of 46 ways to save money.

4) Invest like a Millionaire (Re: Boring)

For you sports fans out there, saving and building cash flow is like your defence. While some would consider defence to be vital for any sports team, they aren’t getting very far without some offence. That’s where investing comes in.

Becoming rich requires not only “defending” ie. saving your cash flow, but also “growing” those savings! This is where the fun begins!

For investors still accumulating for their retirement, one of the easiest, most efficient, and low-cost ways to invest is through All-in-one index ETFs.

Here are some additional ways to index your portfolio.

If you are a little more hands-on with your investments and like the idea of your portfolio generating tax-efficient passive income for your retirement, then check out dividend growth investing. I personally use DSR to help me manage my portfolio and I recommend their services to anyone who’s serious about dividend investing.

Qtrade can help you get started quickly and easily. Using an online brokerage like Qtrade is one of the best ways to help you reach your first million. If starting at 25 you invest a modest $500 per month, you’ll end up a millionaire by the time you are 65.

5) Be Fee-Savvy When It Comes To Investing

In the long run, if you want to become a Canadian millionaire, you should avoid all “expensive” investment opportunities i.e. those that levy heavy fees (whether per transaction or annually).

Once you have a nest egg, it all boils down to compounding interest, and it’s the same way with fees, they compound too.

For example, if your nest egg is $70,000 and you’re able to contribute $10,000 each year, you’ll be a millionaire after 30 years of saving when applying a modest annual return of 5%.

If you have opted for an investment that costs you 1% in fees each year, therefore netting you only 4% annually, you’ll have just $810,000 after 30 years of saving. Fees can make a big difference in your timeline of achieving your financial goals!

Remember to take full advantage of your registered Canadian accounts like the RRSP or TFSA, or the FHSA for saving a first home, as it will help you save more in taxes down the line.

The more your investment portfolio grows, the more important it becomes to choose the right online broker or stock trading app and continuously check and compare your provider’s fees.

6) Make More Income – Start a Side Hustle

Remember earlier when I mentioned that saving was the lowest hanging fruit in building wealth – what if you’re as efficient as you can be with saving? The other side of the coin is to increase your income! Increasing your income to further increase your cash flow for investing will supercharge your wealth.

Is it possible to get a raise from work? What about a side-hustle on something that you enjoy doing? Increasing your income can supercharge your financial goals – at least it did for us!

7) Invest in Real Estate

Investing in real estate is a great hedge against inflation, and can save you money on taxes. By using the Smith Manoeuvre, you can even structure your mortgage so it can be completely tax deductible!

If you haven’t yet bought a home, you should learn about and take advantage of Canada’s tax-free First Home Savings Account (FHSA). It will allow you to save up for a down payment in a tax-sheltered account.

Real estate tends to appreciate in value, meaning it is a great way to increase your net worth. While owning your own home can increase your wealth, owning and renting is the real sweet spot for generating millionaire wealth.

If you live in a location with high home prices, or just don’t have the money for a down payment, Real Estate stocks, or REITs, can provide you with the benefits of owning real estate without the heavy up front investment.

8) Study your Canadian Geography

Canadians seeking to stretch their dollar further can find significant financial relief by opting to live in provinces with a lower cost of living, such as Manitoba, Saskatchewan, and New Brunswick, compared to the high costs associated with Toronto and Vancouver.

The cost of living in Toronto and Vancouver is among the highest in the country, driven up by steep housing prices, higher transportation costs, and pricier day-to-day expenses.

In contrast, many of the Prairie and Atlantic provinces offer much more affordable housing options, lower utility costs, and generally a lower price tag on everyday goods and services. This affordability can lead to a higher quality of life, with more disposable income for savings, investments, and leisure activities.

Additionally, these regions often offer incentives to attract residents, including lower tax rates and various programs designed to encourage migration, further enhancing their appeal to those looking to maximize their financial well-being and get rich in Canada.

With more and more opportunities for remote work, maybe part of your millionaire mindset should be to consider relocating to one of Canada’s hidden (and way more affordable) gems. Just check out this table below comparing housing costs in Canada.

| Province | Avg. Home Price (May 2024) |

| British Columbia | $1,018,279 |

| Ontario | $889,033 |

| Quebec | $511,023 |

| Alberta | $491,962 |

| Nova Scotia | $402,200 |

| Manitoba | $362,535 |

| Prince Edward Island | $355,100 |

| Saskatchewan | $334,500 |

| New Brunswick | $295,500 |

| Newfoundland and Labrador | $290,400 |

9) Utilize Short Term Opportunities

In the current financial landscape of high inflation, you should be deliberate about where you are investing your money in the short term (5 years or less). You don’t want your cash sitting on the sidelines losing value while you wait to use it for a vacation, schooling, a new car, etc.

There are many options for safe short term investing in Canada such as GICs (Guaranteed Investment Certificate), Cash ETFs, and HISAs (High Interest Savings Account).

Money in a GIC is locked away, so you’ll need to plan your timeline wisely if you choose that option. On the other hand, Cash ETFs and HISAs are liquid; you can withdraw the money at any point. This makes them great options as places to hold your emergency fund.

Having an emergency fund saves you from having to sell long term investments or having to utilize your credit card when faced with the unexpected (job loss, health crisis, etc.)

FAQ About How To Become A Millionaire In Canada

The Bottom Line

Listen, I know that starting on your journey to get rich and become a Canadian Millionaire can feel overwhelming, or even impossible. With the current economy and all the variables to consider it’s understandable why some folks never even get started in the first place.

Fortunately, you don’t have to apply every step right away. Just get started on something, and don’t let fear stop you from chasing your dream of getting rich. By managing your money in and out effectively, and sticking to your plan for investing, you’ll be on your way to achieving the esteemed milestone of becoming a “millionaire”.

To get started on your investment journey, read our Qtrade review, and find out why they are the top rated online brokerage in Canada. This will set you on your path to becoming a millionaire in Canada!

Best 2026 Broker Promo

Up To $2,000 Cash Back + Unlimited Free Trades

Open an account with Qtrade and get the best broker promo in Canada: $100 when you invest $1,000!

The offer is time limited - get it by clicking below.

Must deposit/transfer at least $1,000 in assets within 60 days. Applies to new clients who open a new Qtrade account by July 31, 2026. Qtrade promo 2026: CLICK FOR MORE DETAILS.

this is an old post