Net Worth Updates

Million Dollar Journey’s net worth updates – follow our path to success and becoming rich in Canada.

Most Popular

Financial Freedom Update (Q3) 2021 – Sequence of Returns Risk Edition

Welcome to the Million Dollar Journey 2021 (Q3) Financial Freedom Update – the third update of the year! If you would like to follow my…

Financial Freedom Update (Q2) 2021 – Portfolio All-Time High Edition

Welcome to the Million Dollar Journey 2021 (Q2) Financial Freedom Update – the first update of the year! If you would like to follow my…

Most Recent

How to Become a Millionaire in Canada

I am sure that most of us out there have wondered what’s the quickest way to get rich in Canada. While we don’t advise getting…

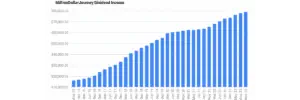

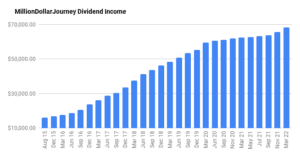

Financial Freedom Update Nov 2023 – $78.8k in Dividend Income!

Welcome to the Million Dollar Journey November 2023 Financial Freedom Update – the third update of the year! If you would like to follow my whole financial…

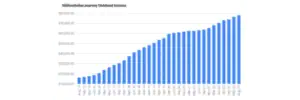

Financial Freedom Update Aug 2023 – $77.8k in Dividend Income!

Welcome to the Million Dollar Journey August 2023 Financial Freedom Update – the second update of the year! If you would like to follow my whole financial…

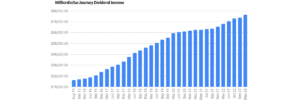

Financial Freedom Update May 2023 – First Update of the Year ($73.8k in Dividend Income!)

Welcome to the Million Dollar Journey May 2023 Financial Freedom Update – the first update of the year! If you would like to follow my whole financial…

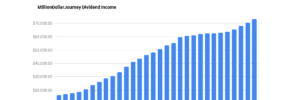

Financial Freedom Update Oct 2022 Update ($73k in Dividend Income!)

Welcome to the Million Dollar Journey Oct 2022 Financial Freedom Update – the third update of the year! If you would like to follow my whole financial…

Financial Freedom Update March 2022 – First Update of the Year ($68,100 in Dividend Income!)

Welcome to the Million Dollar Journey March 2022 Financial Freedom Update – the first update of the year! If you would like to follow my whole financial…

Financial Freedom Update Sept 2021 – Market Highs Edition

Welcome to the Million Dollar Journey September 2021 Financial Freedom Update – Market Highs Edition! If you would like to follow my whole financial journey, you can…

Financial Freedom Update (Q3) 2021 – Sequence of Returns Risk Edition

Welcome to the Million Dollar Journey 2021 (Q3) Financial Freedom Update – the third update of the year! If you would like to follow my…

Financial Freedom Update (Q2) 2021 – Portfolio All-Time High Edition

Welcome to the Million Dollar Journey 2021 (Q2) Financial Freedom Update – the first update of the year! If you would like to follow my…

"I've completed my million dollar journey...

Want some help with yours?”

Instantly download our free eBook on tips for how to organize your RRSP, TFSA, and other investments, in order to get the most out of your retirement at any age.

")